Day 1 and $106,102…..

Six-Figures Under

Welcome to the Dollar 15 blog and the journey from $100k in student loan debt, to freedom. In August of 2013, I walked into my first day of business school at Southern Methodist University’s (SMU) Cox School of Business bright-eyed and full of dreams of career advancement, a six figure salary, and a corner office. SMU, otherwise known as “Southern Millionaire’s University”, is also known for one of the best, but most expensive, business schools in the country. Greek life makes up over 40% of the student body population, and the standard male wardrobe is made up of popped collar Ralph Lauren polos, dockers, and the loafer of choice. Every year America’s southern elites file into SMU by the thousands. I spent two years studying with the children of the country’s CEOs and oil tycoons. I spent much of my free time working part-time jobs and wondering why I didn’t have parents that could write me five-figure checks to cover the year’s tuition and make me an authorized user on their American Express black card. Two years later, I would graduate with my MBA, an offer to join one of the nation’s best leadership programs, a decent salary, and almost $100k in debt.

Now I’m sure you’re wondering, “who is this chick, what is she writing about, and why does she think we care?” Allow me to introduce myself. I’m the chick who spent 2 years away from the work force, missing out on over $100k in earnings, only to borrow $100k, to get a job that pays me about what the principle on my loan is. Cool. But the real issue is, since graduating in May of 2015, I’ve made 8 loan payments, only to see my loan balance capitalize and GROW! After watching my relaxed efforts to repay my debt get me nowhere, I decided to get serious about this thing. So Tyrone and I started this blog because we want to document my journey to freedom as a method of keeping myself honest and accountable.

Wait, who the hell is Tyrone? I’m glad you asked. Tyrone is my debt in its entirety. Tyrone was named after the friend of the nameless man on the other end of Erykah Badu’s 1997 piece “Tyrone.” I named my debt Tyrone because like Badu’s lyrical picture, Tyrone is ALWAYS around, but never really there for any particular purpose. Tyrone “don’t never have to pay, don’t have no cars, hang around in bars try to hang around with stars.” Tyrone is the homie of a homie who you only deal with because of the mutual friend connecting the two of you. In this case, my MBA is the homie, Tyrone is the homie of that homie that comes by every few weeks to ask me for “a couple dollars”.

To further introduce myself, my name is Marlissa Collier, and my student loan just won’t let me be great. I’m a Los Angeles native currently living and working in Dallas for a technology and media company as a mid-level manager. I’m 28 years old, grew up economically and socially disadvantaged and somehow got two degrees from two pretty good universities. And when I say “somehow got two degrees”, that’s not a sideways way of being cocky or overly proud of myself for “making it out the hood”, that’s really me saying that I’m still flabbergasted by all of the opportunities that have come my way. But anyway, back to the matter at hand. I graduated with close to $100k in debt and after compounding, Tyrone is currently $106,102! And you thought your man troubles were serious?

Let me be honest up front. I do make a decent salary. So I do have the wiggle room in my budget that allows me the freedom to take on the task of ridding myself of a large amount of debt. I do not use my new tax bracket as an excuse to live hood rich. “What’s hood rich“, you ask? Well, if you managed to finance the Beemer by putting it in your Grandma’s name because you have terrible credit, that’s hood rich. If you bought a Hummer but never have money for gas, that’s hood rich. If you live in your mama’s house without paying her any rent but come in the club buying bottles every weekend, that shit is hood rich as hell. That’s not me. I tend to be very careful about where I spend as I come from very humble means, have worked since I was 15 years old, and was turned into a hustler by my Grandma very early in life. In essence, I live within, and at times below, my means. So to review, my debt is made up of only student loans, my income is decent, and my spending habits are responsible.

I stated earlier that I’ve made 8 monthly payments since December of 2015 only to see my balance increase. Say hello to the magic that is compounding interest. And what’s worse is, this fuck shit is legal! I like to call it the cost of being poor. Because student loan interest is typically compounded daily, which means your interest rate is divided by the number of days in the year and you are charged daily based on the outstanding balance that day, it can certainly feel like you aren’t making any progress once that new interest is applied to your balance.

Annoyed, frustrated, and essentially pissed off yet? Cool. I too have decided that enough is enough. After combing through each of my loans, I realized that on my current 10 year standard repayment plan, I wouldn’t get rid of this loan until I was almost 40 years old. See how that works? 28 years old +10 years in repayment =38 years old =almost 40 years old.

Forty. Years. Old! That could mean delaying saving for retirement, traveling, marriage, having children, and living the lifestyle that I had in mind when entering business school. Then, conjuring my basic excel skills, I calculated the amount of interest I would pay if I continued on this path. When $36,904 on top of my principal balance was spit in my direction, I knew I had to make some moves.

This journey won’t be an easy one. I don’t have a ton of cash saved up, I have no one I can borrow from, my trust fund is nonexistent, investments are limited to my company provided 401K, and my annual salary after tax is less than the principle of my loans. I’ve heard of people ridding themselves of debt in 7 months, but let me paint my picture. I’m one of few in my family to earn a living that allows me to have a little discretionary income, and therefore I help out back home. Not to mention that my niece’s dream of becoming a concert violinist is very important to me. I also take care of all of my expenses as I was not fortunate enough to have parents that can help me with anything financially. I take care of myself, and sometimes others, therefore it’s not possible for me to throw every extra dime at my debt.

Knowing this, I took an honest look at my finances and decided that I could set a target for debt freedom at 36 months. This extended timeline will mean cutting expenses, doubling monthly payments, and using tax returns, bonuses, and salary increases to pay down my debt over the next 3 years. I’m not even sure if I’ll succeed at this, but I’ll damn sure try. I look forward to you following this journey and I hope that I can inspire others being haunted by our country’s debt crisis to also become financially free. Make sure to reach out on Instagram and Twitter @blkgyrlfly

State of the Debt

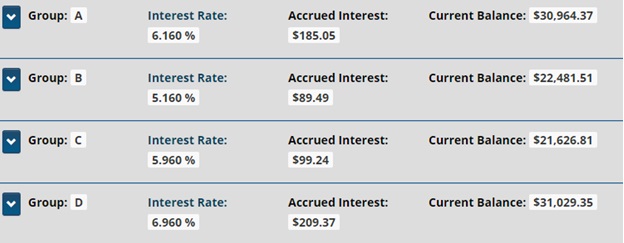

My NelNet student loan statement as of 9/14/2016. It’s not pretty. $106,099.04

[…] I take you all on my journey from Six-Figures Under to debt freedom, I figured I should also share my strategy. But before I share my actual debt […]